PCCA Cotton Market Weekly 02-May-2025

Posted : May 03, 2025

May 2, 2025

The cotton market posted five consecutive days of losses, weighed down by weather and broader market headwinds. Although the trade war continues, there are signs that tariff relief may be on the horizon. Still, the ongoing conflict contributed to disappointing economic data throughout the week. With so much uncertainty in play, what’s next for the cotton market? Get QuickTake’s read on the week’s events in five minutes.

Although the rain in West Texas was much needed, it pressured the market this week, reversing the gains seen last week.

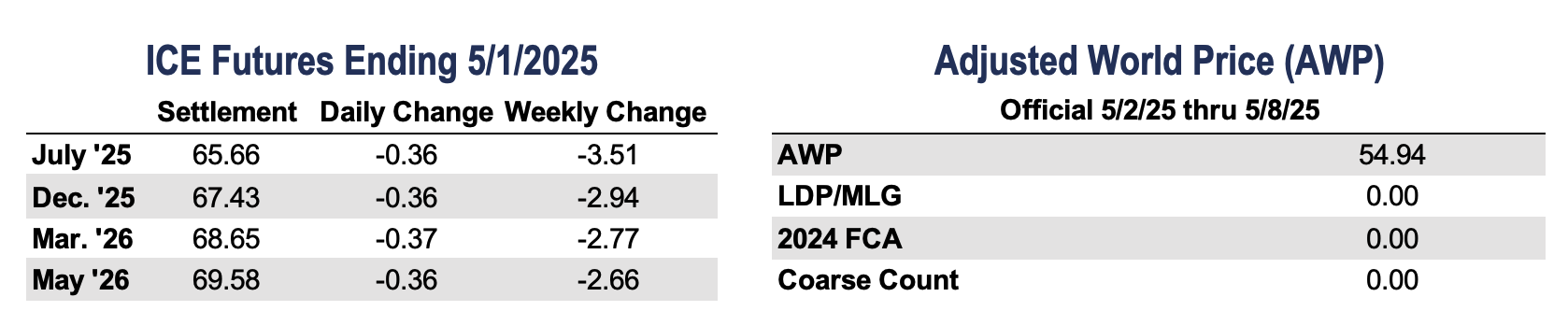

- July futures slid 351 points for the week, settling at 65.66 cents per pound.

- The cotton market closed lower in all five trading sessions this week. While technical and fundamentals remain weak, light trading volume due to global holidays and rainfall in West Texas contributed to the decline. Although the moisture was desperately needed in the Southwest, the market interpreted it as a signal for improved crop prospects, adding to concerns about rising stocks in an already oversupplied global market.

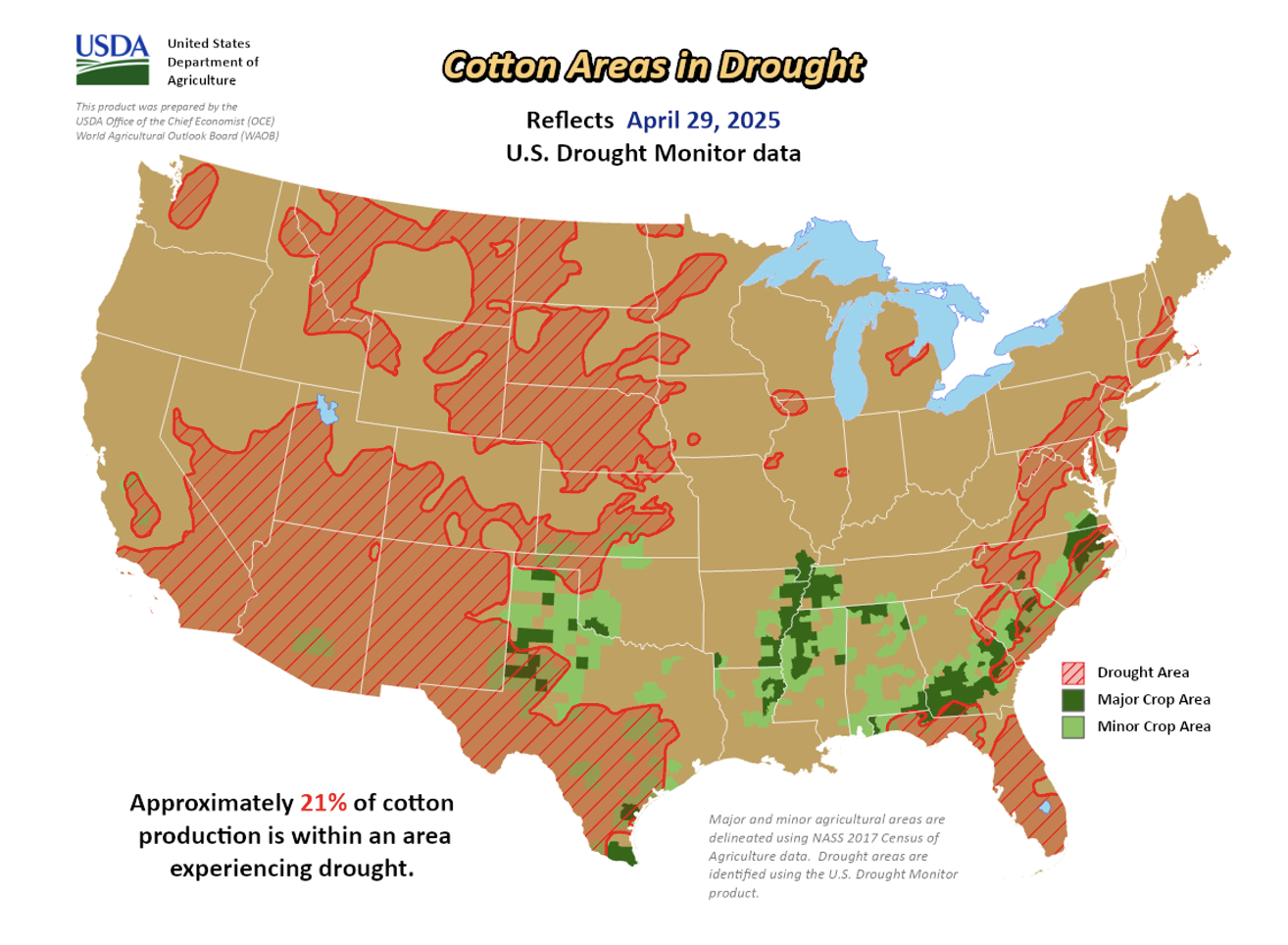

- Planting in Texas is slightly ahead of the five-year average, with 21% of the crop estimated to be planted. South Texas has made steady progress and picked up some moisture over the past week, which may have caused slight delays but has generally supported crop development. West Texas, Oklahoma, and Kansas also received precipitation, which was often accompanied by thunderstorms and severe weather but should aid planting efforts and help replenish soil moisture.

- Trading volumes were light, as many countries were on holiday throughout the week, and open interest decreased by 6,949 contracts to 213,513. Certified stocks held steady at 14,478 bales.

Strong tech earnings lifted stocks this week, but market sentiment remains shaky amid mixed economic data and ongoing trade war uncertainty.

- Stock markets declined after news broke that the U.S. economy contracted in the first quarter, defying expectations for modest growth. GDP fell 0.3% from the previous quarter, compared to forecasts of a 0.2% increase, marking the first decline since 2022. Much of the weakness is tied to trade war uncertainty, as U.S. importers rushed to stock up on foreign goods ahead of incoming tariffs.

- According to the Conference Board, consumer confidence fell to 86 this month, the lowest reading since May 2020 and the fifth straight monthly decline. Ongoing concerns about tariffs and the trade war continue to weigh on the economic outlook. Given the uncertainty around trade policy and broader economic trends, the Fed is expected to keep interest rates unchanged at its upcoming meeting on May 6 and 7.

- Crude oil prices declined this week as the U.S. dollar strengthened. Fears of rising production and oversupply were the primary drivers behind the drop in oil prices. Despite weaker economic data, the dollar rallied on speculation that new trade deals may be in the works. While still unconfirmed, even talk of negotiations was enough to lift the currency, adding yet another headwind for commodities.

- The U.S. and Ukraine signed a mineral deal this week, even as tensions around the war with Russia persist. The agreement establishes joint management and revenue sharing from Ukraine’s mineral reserves, with equal voting rights for both countries. Although Ukraine will maintain legal authority, U.S. companies are expected to access its critical mineral sector.

- The U.S. added 177,000 jobs in April, surpassing expectations and signaling robust job growth. The unemployment rate remained unchanged at 4.2%, although job gains from February and March were revised lower.

U.S. export sales held steady, while shipments were strong for the week ending April 24.

- For the 2024/25 marketing year, U.S. merchants booked 108,400 Upland bales and shipped 366,000, with new crop sales totaling 32,900 bales. Despite tariff-related uncertainty, business continues, with steady, although smaller, volumes sold to importers. Sales and shipments remain above the pace needed to meet USDA’s lowered export estimate of 10.9 million bales, which has already been surpassed in total commitments. Demand will likely stay muted until there’s more clarity on trade policy.

- Pima merchants booked 13,900 bales and shipped 3,900, keeping Pima sales and shipments above the pace needed o reach USDA’s estimates.

The Week Ahead

- Trade policy and economic concerns will remain in focus next week, along with the Federal Open Market Committee’s interest rate decision on May 6–7. Otherwise, economic data is expected to be relatively quiet in the week.

- The World Agricultural Supply and Demand Estimates (WASDE) Report will be released on Monday, May 12, at 11:00 a.m. CST, offering the first official forecast for the 2025/26 crop year. USDA will base its production estimates on the March Prospective Plantings Report, which pegged U.S. cotton acreage at 9.867 million acres. In the Southwest, Texas accounted for 5.527 million acres, Oklahoma 413,000, and Kansas 140,000. Recent weather has been favorable, which could support a larger crop despite reduced acreage. Still, with May typically being the wettest month and summer weather often unpredictable, the 2025 crop size remains uncertain.

Announcements

New Grower Enrollment for Better Cotton will be open March 3-May 30, 2025. For assistance or questions about enrolling in this program, contact PCCA at 806-763-8011.

The Seam

As of Thursday afternoon, grower offers totaled 44,053 bales. During the week, 1,859 bales were traded on the G2B platform with an average price of 63.14 cents per lb. The average loan was 50.85, which resulted in a premium of 12.29 cents per lb. over the loan.