PCCA Cotton Market Weekly 23-May-2025

Posted : May 24, 2025

May 23, 2025

With headline risk subdued and few data releases, cotton prices were little changed. With uncertainty around tariffs and global developments still looming, where will cotton prices go from here? Get QuickTake’s read on the week’s events in five minutes.

Following a choppy week, cotton prices finished nearly flat, staying within one of the narrowest trading ranges of the year — just 164 points.

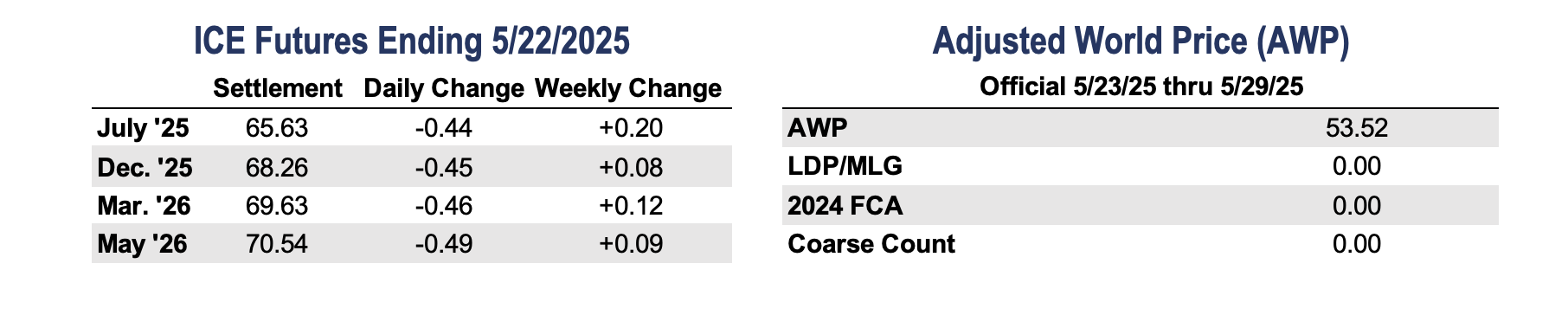

- July futures increased 20 points on the week, settling at 65.63 cents per pound.

- It was a relatively quiet week for the cotton market, which continued to take its cue from outside influences. July futures hovered around 66.00 cents per pound, with little news to drive movement in either direction. New crop demand for the December contract remains soft amid current price levels and ongoing tariff concerns.

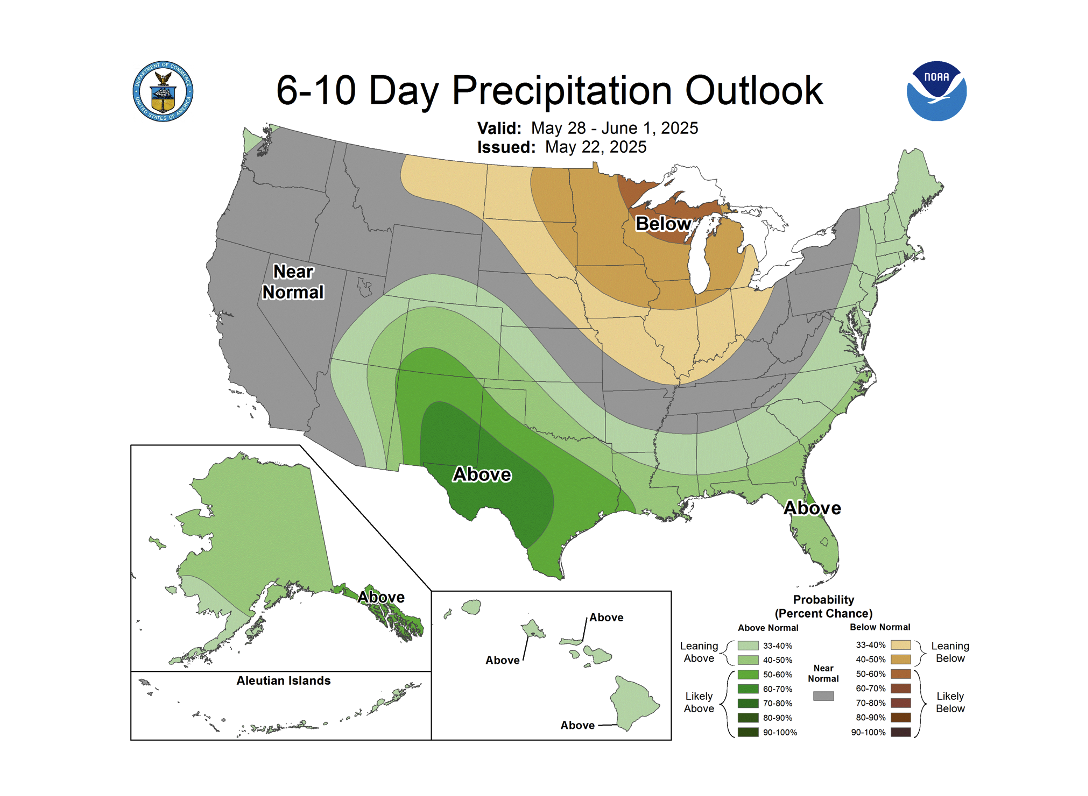

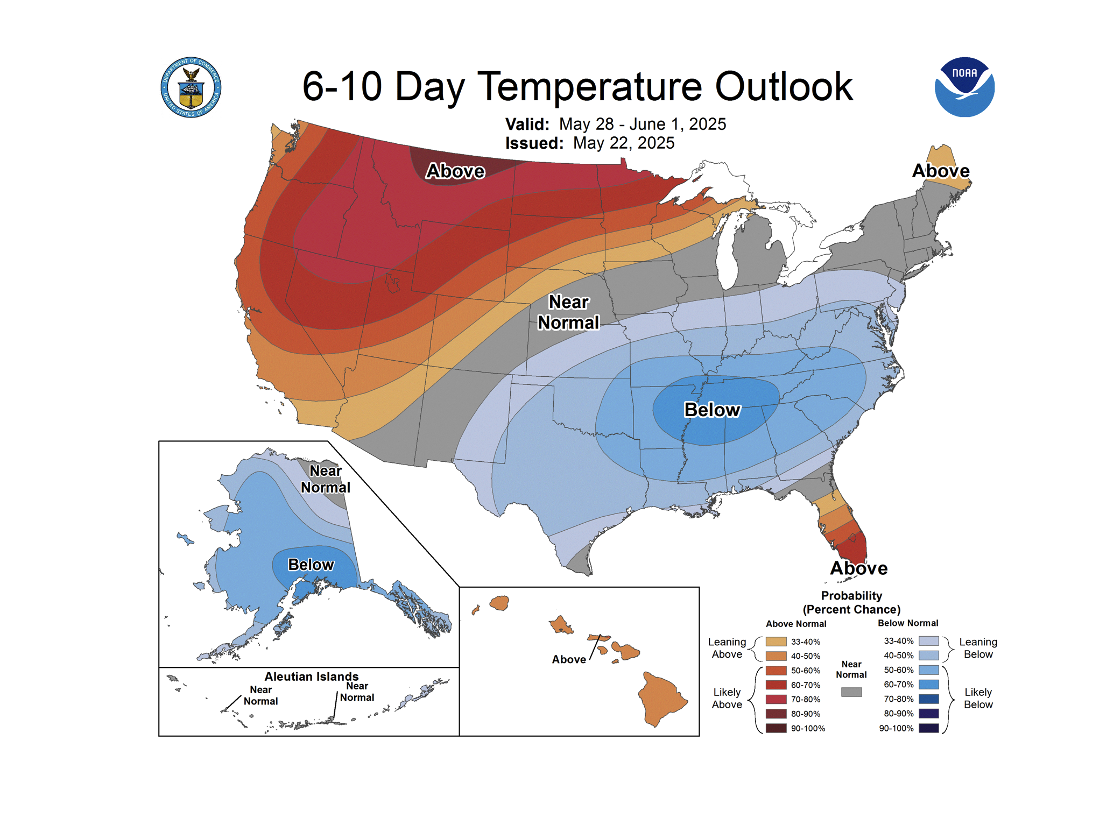

- Planting is well underway across the Southwest. While Texas lags slightly, Oklahoma and Kansas remain ahead of the 5-year average, according to USDA’s Crop Progress Report. This week, unseasonably hot and dry conditions favored planting in West Texas, Oklahoma, and Kansas. Rain will be needed in the coming week to support emergence and crop development, especially in South Texas. There are concerns that planted acreage across the Cotton Belt will fall short of the 9.87 million acres projected in USDA’s Prospective Plantings report.

- Trading volume was lighter this week, while open interest rose by 6,851 contracts to 235,093. Certified stocks increased to 39,796 bales with 6,696 new certifications.

Stock markets saw their biggest sell-off of the month after Moody’s downgraded the U.S. credit rating, and rising bond yields rattled investors, though some losses were recovered by week’s end.

- Anxieties were high this week after Moody’s downgraded the U.S. debt rating to Aa1 (next to highest) from Aaa (the highest), pushing bond yields higher and making stocks less attractive. While equities have held up since the announcement of the 90-day tariff pause, volatility has persisted. According to Moody’s, “Over more than a decade, U.S. federal debt has risen sharply due to continuous fiscal deficits. During that time, federal spending has increased while tax cuts have reduced government revenues. As deficits and debt have grown, and interest rates have risen, interest payments on government debt have increased markedly.” Practically, U.S. sovereign debt is still rated among the highest, but bond traders lowered their valuations of U.S. debt, which raised interest rates. Ultimately, that will increase the borrowing costs, which is bad news for leveraged industries like agriculture.

- The House of Representatives passed a sweeping tax and spending bill that extends expiring tax cuts, introduces new ones, and reduces spending on Medicaid and nutrition assistance. The bill now heads to the Senate, where revisions are expected. Despite skepticism about its scale, lawmakers pushed through ‘one big, beautiful bill’ ahead of the Memorial Day deadline. While spending cuts are generally positive in the eyes of the bond market, the bill still adds a projected $3.3 trillion to the country’s debt over ten years.

- The bill also contains measures to increase the ARC/PLC reference price of seed cotton to 42¢ per pound, more than 14%. If the Senate approves the provision, the new price will apply to 2025-crop cotton.

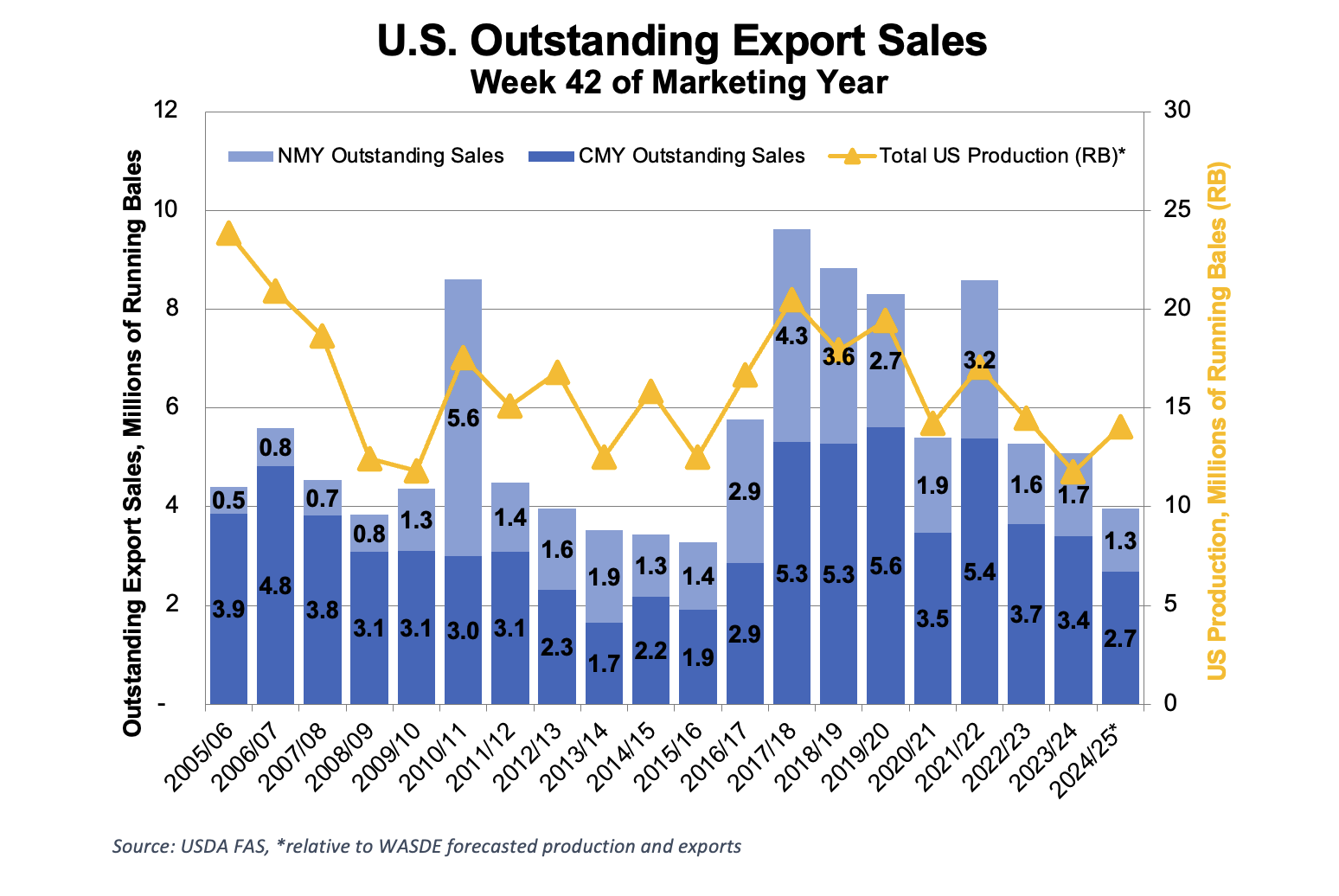

U.S. export sales were surprisingly strong, and while shipments slowed, they remain above the pace needed to meet USDA’s export target.

- For the 2024/25 marketing year, U.S. merchandisers booked 141,400 Upland bales and shipped 251,500, with new crop sales totaling just 7,400 bales. Sales were stronger than expected, and total commitments remain above 100% of the current crop. While shipments slowed, they’re still above the pace needed to meet USDA’s 11.1 million bale export estimate. However, new crop sales were notably weak, hitting their lowest since 2016.

- Pima sales improved from last week, with 9,700 bales booked and 7,600 shipped—both remaining ahead of the pace needed to meet USDA projections.

The Week Ahead

Next week will bring a slight uptick in data releases compared to this week. Markets will be closed Monday, May 26, but barring headline risk, key updates on Consumer Confidence, GDP, and Personal Income are expected. Delayed reports on Crop Progress and Export Sales will also be released for cotton.

The Seam

As of Thursday afternoon, grower offers totaled 41,649 bales. During the week, 1,682 bales were traded on the G2B platform with an average price of 60.87 cents per lb. The average loan was 53.42, which resulted in a premium of 7.45 cents per lb. over the loan.