PCCA Cotton Market Weekly 06-Jun-2025

Posted : June 07, 2025

June 6, 2025

Markets were active this week, with cotton holding steady in a narrow range as traders watched mixed weather conditions, strong export shipments, and ongoing trade news. With key reports and inflation data on the horizon, where do prices go from here? Get QuickTake’s read on the week’s events in five minutes.

The summer doldrums have set in, leaving cotton futures stuck in a narrow range. Prices ended the week slightly higher, supported by encouraging export sales and some positive developments on the trade front.

- July futures rose a modest 52 points during the week, settling at 65.36 cents per pound.

- The market remains rangebound as the largest of the indexes begins to roll. Meanwhile, the Southwest received some much-needed rain, providing a bit of optimism for growers. With First Notice Day quickly approaching and options set to expire in just a week, traders are closely watching developments. Despite the broader uncertainty, there have been inquiries for both old and new crop U.S. cotton.

- Trading volume was slightly heavier this week, with open interest increasing by 395 contracts to 238,450. Certified stocks rose to 53,700 bales, including 11,837 new certifications.

Stocks wavered after President Trump and Elon Musk clashed over the “One Big, Beautiful Bill,” but managed to recover by the week’s end.

- After initially joining forces during the presidential campaign, Donald Trump and Elon Musk soon found themselves at odds over the spending bill making its way through Congress. Musk voiced concerns that the bill would balloon the deficit and raise the debt ceiling. The legislation also proposed cuts to the electric vehicle mandate—a blow to Musk, given Tesla’s reliance on federal subsidies, which Trump then targeted in retaliation. A heated back-and-forth unfolded on social media, though tensions seemed to ease somewhat after Tesla’s stock dipped, weighing on the broader market and sparking some disagreement over the budget.

- After weeks of stalled negotiations, the U.S. and China have agreed to resume trade talks, with Presidents Trump and Xi appearing to set aside their latest disagreements and revive the “truce” met in Geneva. However, traders remain cautious after Trump’s comments that it is “extremely hard” to strike a deal with Xi and his reminder of the deadline for other countries’ best offers. Nonetheless, both cotton and equity markets moved higher. A trade agreement between the U.S. and China would benefit the U.S. cotton market, as China is typically its largest buyer.

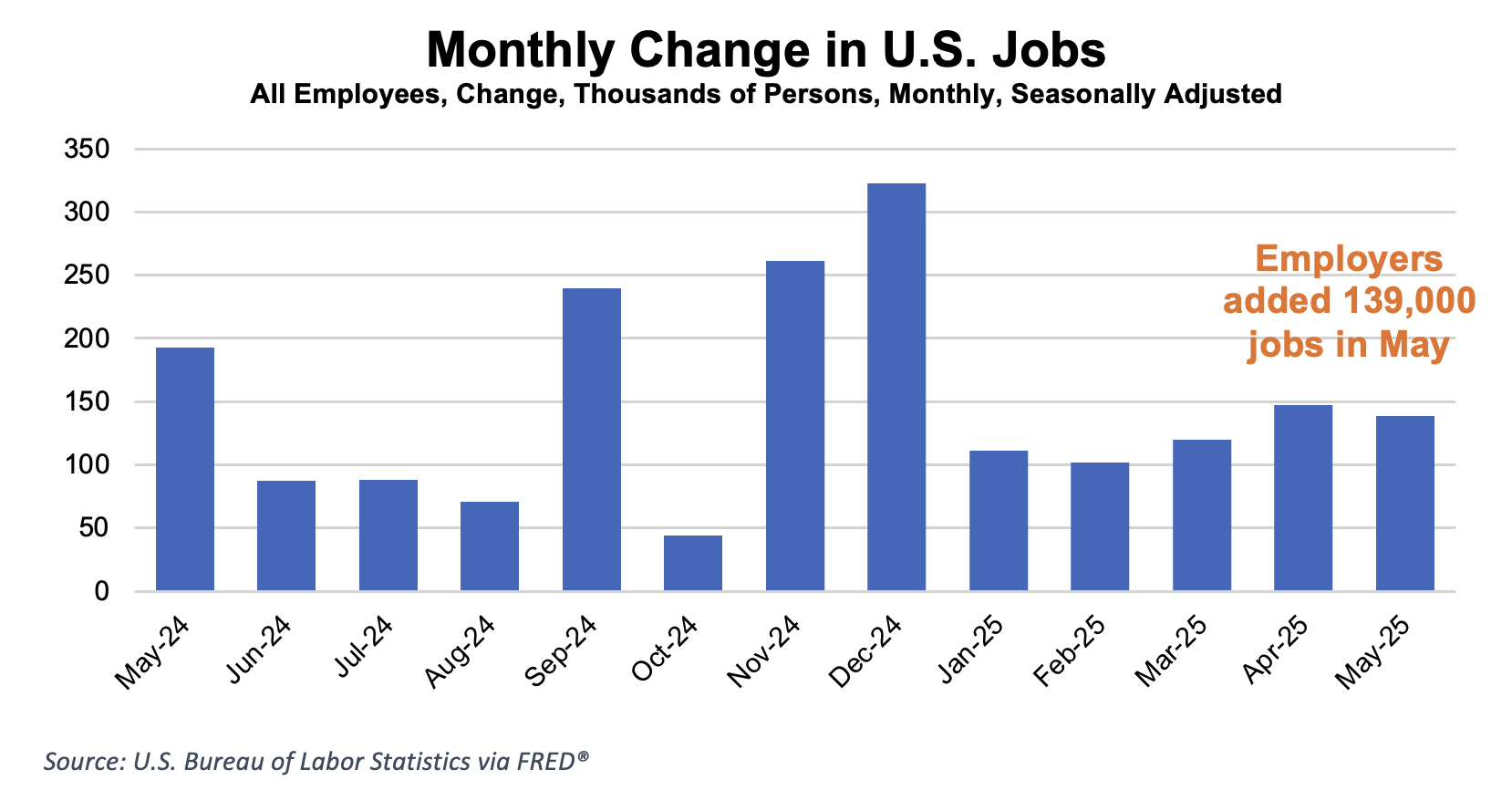

- Jobs data took center stage this week. Private-sector payrolls added only 37,000 jobs in May, the lowest in over two years, which made markets hesitant about the upcoming nonfarm payrolls report. However, nonfarm payrolls beat expectations with a gain of 139,000. March and April data were sharply revised. The unemployment rate held steady at 4.2%. Although job growth has slowed, it continues amid recent economic turmoil from tariffs. This gave the Fed some breathing room ahead of its June 17-18 meeting.

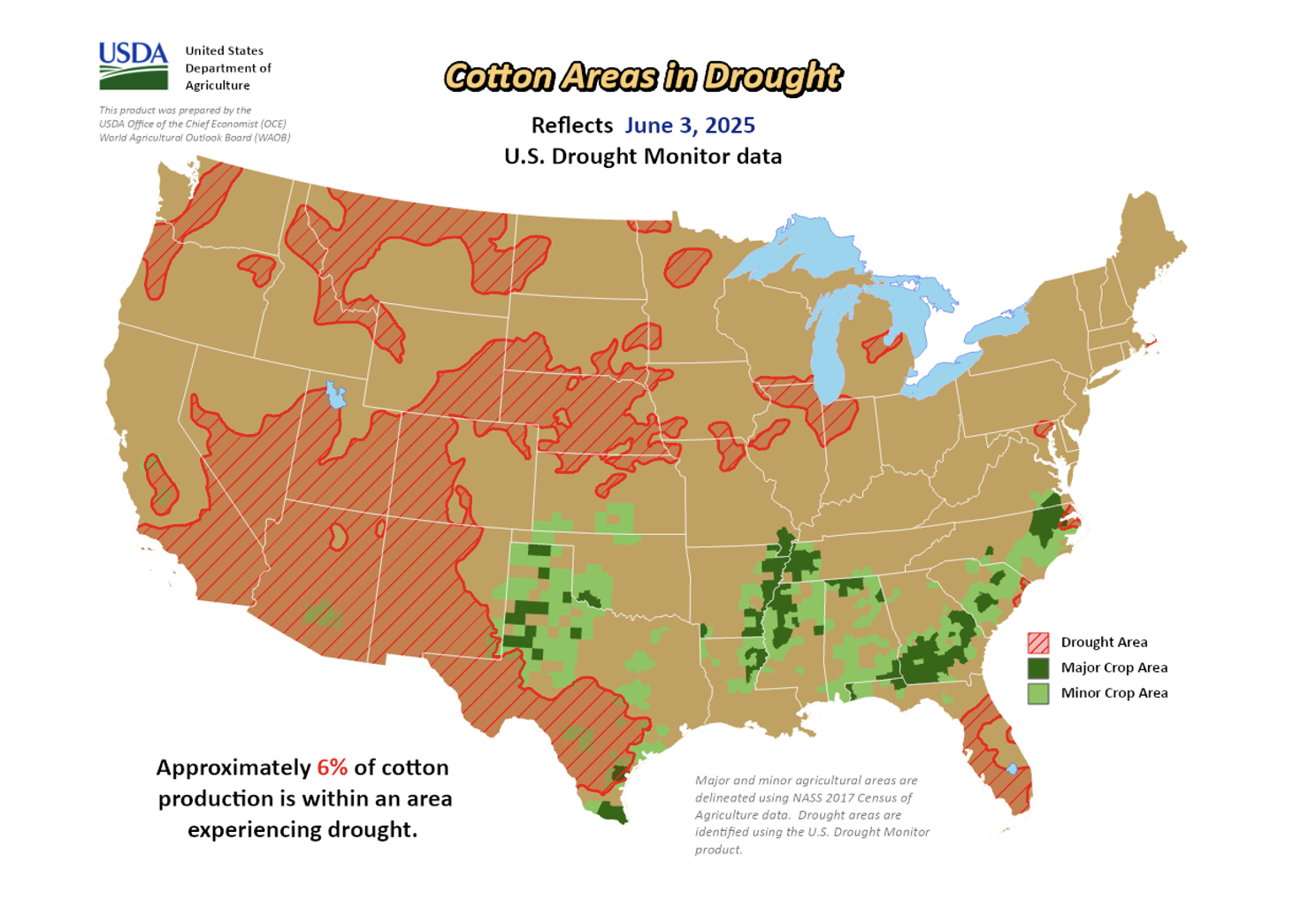

U.S. planting is progressing steadily, with 66% of the crop planted, though crop conditions vary widely across the Cotton Belt.

- In the Southwest, Texas is 61% planted, Oklahoma 40%, and Kansas 82%—all at or slightly above the 5-year average. However, concerns remain in parts of Texas (particularly the Panhandle) and Kansas, where unusually cold days and a lack of sustained warmth have prevented crops from emerging and slowed growth.

- In Texas, 20% of the crop is poor or very poor, with 40% fair. Oklahoma is in better shape, with 7% poor or very poor and 25% fair. Kansas shows the strongest conditions, with just 4% poor or very poor and 27% fair. Despite the concerns about cooler-than-average temperatures and slow emergence, the overall picture is mixed but not alarming.

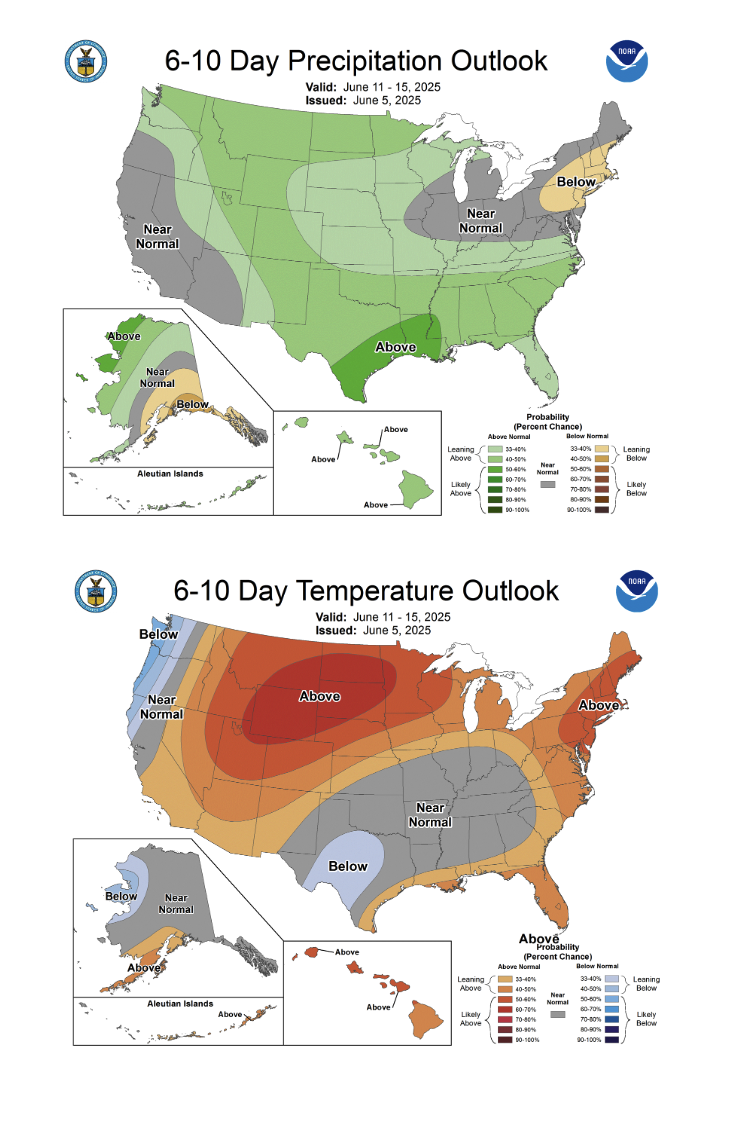

- Weather has taken center stage in recent weeks. Scattered storms have rolled across the Southwest, often bringing severe conditions. Despite these storms, drought-free conditions have generally prevailed in West Texas, Oklahoma, and Kansas. As final planting dates pass or near, growers hope for more sunshine and warmth, as dryland planting seems to be running behind schedule. South Texas has enjoyed mostly favorable weather this week, though some areas could still use more rain to support plant development.

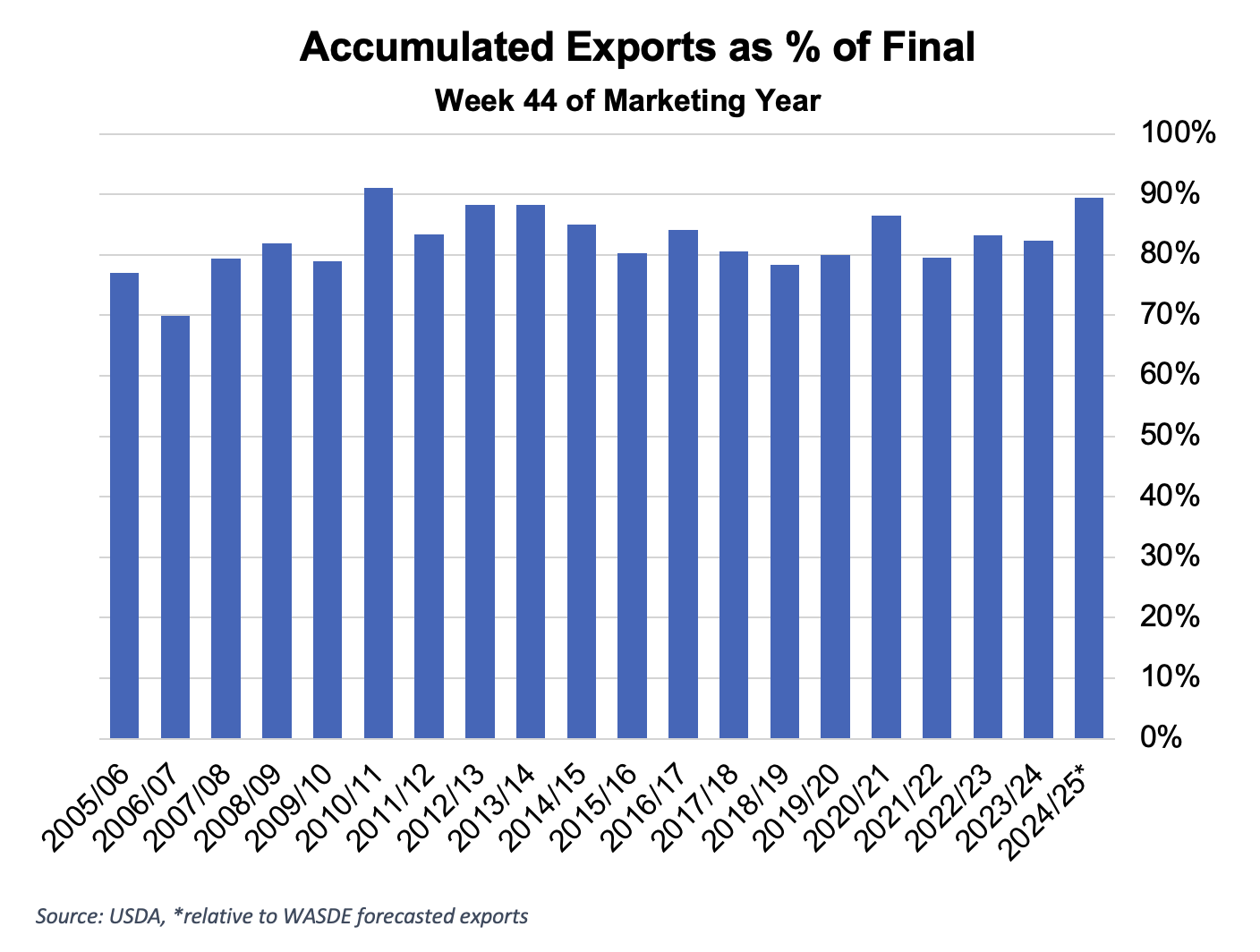

U.S. export shipments remained strong this week, rising 15% from the week prior and staying well above the pace needed to meet USDA’s export target.

- For the 2024/25 marketing year, U.S. merchandisers booked a net 109,800 Upland bales and shipped 316,100, with new crop sales totaling 39,000 bales. Sales were lower but still higher than needed, and total commitments continue to remain above 100% of the current crop. Shipments increased from the previous week, which provided support to the market on Thursday. Exports are still above the pace needed to meet USDA’s 11.1 million bale export estimate.

- Pima sales fell from the previous week, with merchandisers booking 6,700 bales. However, shipments rose 66% to 11,100 bales exported.

The Week Ahead

Next week will be busy, with updated supply and demand estimates released on Thursday, June 12 at 11:00 a.m. CST. We’ll also get the usual cotton updates in the Crop Progress and Condition Report and the U.S. Export Sales Report. Additionally, key inflation data will be released, including the Consumer Price Index (CPI) and Producer Price Index (PPI).

The Seam

As of Thursday afternoon, grower offers totaled 37,107 bales. During the week, 1,043 bales were traded on the G2B platform at an average price of 64.26 cents per lb. The average loan was 53.35, which resulted in a premium of 10.91 cents per lb. over the loan.